Covid-19 may seem to colour everything in transport right now but other things are happening. HS2 Phase One, the route between London and the West Midlands, reached a milestone last month with the Government issuing the notice to proceed for construction. Although that made headlines, the revised business case for Phase One released on the same day received much less attention.

Even here Covid-19 makes an appearance, though the analysis was prepared before the outbreak began. The Department says it considered whether it was right to proceed with construction, given the circumstances. “In line with public health guidance, which allows construction activity to continue where it is safe to do so, we have concluded that continuing is the right course of action.” On the bigger question of the virus’s possible long-term impact on travel demand, the Department says: “The uncertain outcome of the Covid-19 outbreak means it has not been possible to undertake specific analysis to determine the outbreak’s potential longer-term impacts to transport passenger demand.”

The London to West Midlands HS2 route will be designed to allow trains to operate at 330kph (206mph) routinely, with a maximum speed of 360kph (225mph). HS2 trains will run on the conventional network at speeds of up to 177kph (110mph).

Phase One is expected to cut the journey time from London to Birmingham from 82 to 49 minutes. Journey times to the northwest of England and Glasgow will also be cut, with these further benefitting from the Government’s plan to build phase 2a (West Midlands to Crewe) to the same timescale.

With the full Y-network in place to Manchester and Leeds, the London to Manchester journey time will be cut from 127 to 67 minutes and Birmingham to Leeds from 118 down to 49.

The cost of Phase One is now put in a range of £35bn-£45bn (Q3 2019 prices). The lower end of the range (actually £34.7bn) is the point estimate, £40bn is the target cost (including £5bn of contingency), and £45bn the project’s funding envelope agreed with the Treasury.

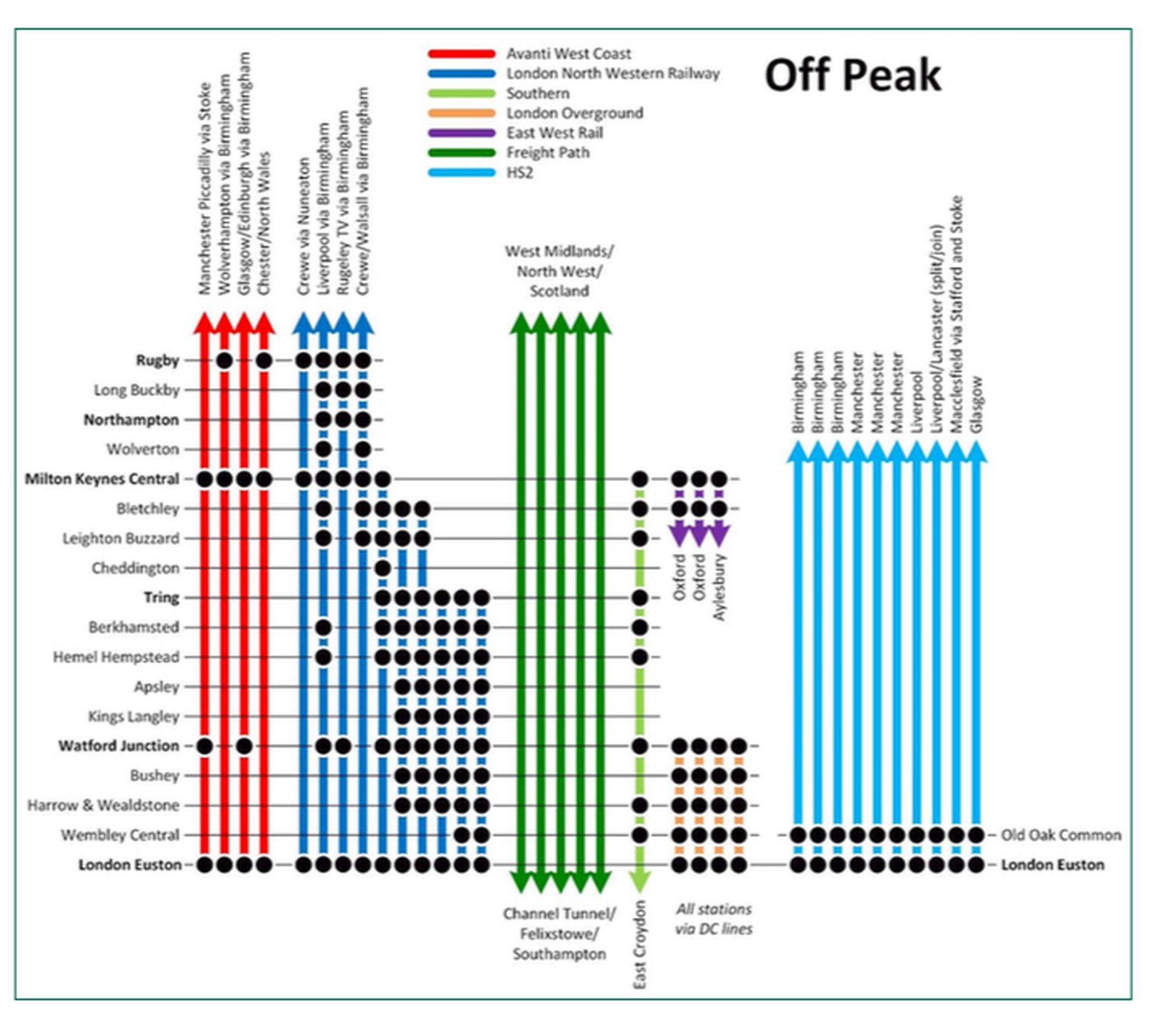

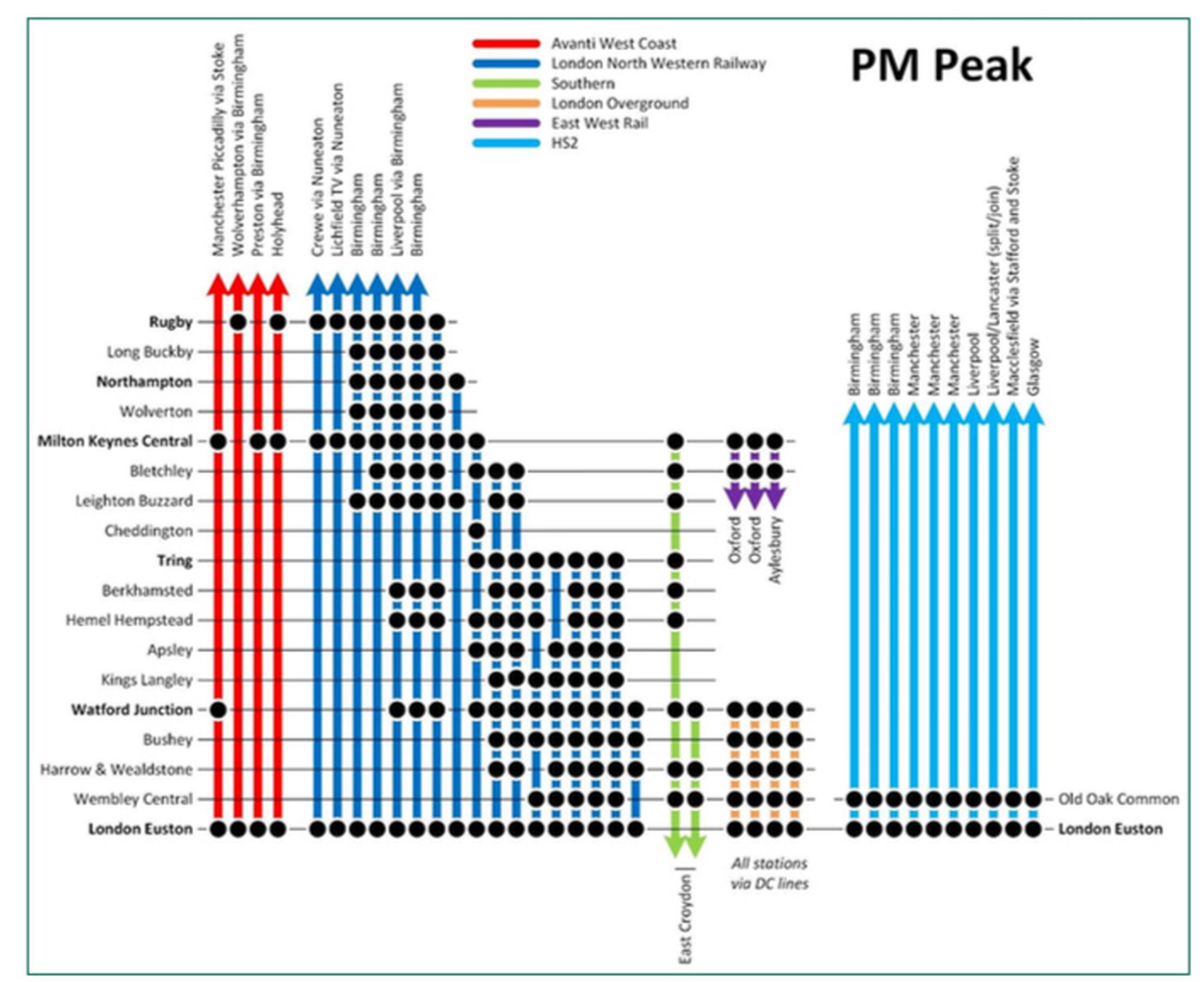

Phase One is now expected to open in stages, with services initially running between Birmingham Curzon Street and Old Oak Common in west London. “This will ensure that the time required to get an optimised solution for a terminus at Euston does not delay the start of HS2 services,” the DfT explains. Services are expected to commence between 2029 and 2033.

A maximum of six trains an hour will operate from Old Oak during this interim period, comprising three trains per hour between Old Oak and Curzon Street, and one train an hour to Liverpool Lime Street, one to Manchester Piccadilly and one to Glasgow Central. The latter three services would run over the HS2 phase 2a line as far as Crewe, where they would join the conventional network.

Service frequencies would rise to ten an hour when the Euston HS2 station opens: three to Birmingham; three to Manchester Piccadilly; two to Liverpool Lime Street (one of which would also serve Lancaster, the two portions splitting/joining at Crewe); one to Glasgow Central; and one to Macclesfield. All trains going north of Birmingham would use phase 2a to Crewe with the exception of the Macclesfield service that would use the Handsacre Junction connection to the West Coast Main Line and serve intermediate stops at Stafford and Stoke. The economic case for Phase One assumes that services from Euston commence in December 2031.

HS2 Phase 2b, the lines between Crewe and Manchester and the West Midlands to Leeds are now wrapped up in the Government’s review of the rail needs of the Midlands and north of England. Assuming Phase 2b is completed as currently planned, then the Government envisages the number of train services running over Phase One rising to 17 trains per hour each way:

In addition, services are assumed to run from Birmingham to: Edinburgh/Glasgow; Manchester; Leeds; and Newcastle.

The rolling stock requirements for HS2 envisage a fleet of 54 trains capable of also running on conventional lines, and an option for up to 30 more. The initial fleet provision includes enough trains to service the currently proposed Phase One and 2a train service specification. Trains would be 200 metres long but could operate as double formations.

The business case contains the five standard cases required by the Treasury: the strategic, financial, economic, commercial and management cases.

In the strategic case, the DfT says the rationale for building HS2 has strengthened with time. The need for the project has been restated at key milestones in the project: in 2013 alongside deposit of the Phase One Hybrid Bill, and in 2015 and 2017.

“At each point an increasing weight of evidence has demonstrated the pressing importance for a step change in capacity to alleviate crowding problems on the existing railway, and the scheme’s potential to redistribute opportunity and prosperity more evenly across the country,” says the Department.

It says the key justifications for building HS2 are:

Moreover, HS2 will also play “a vital role in delivering the Government’s net zero [greenhouse gas] objectives”

On capacity, the DfT says rail passenger growth has averaged 3.7 per cent a year since the mid-1990s, and long-distance passenger demand has grown at 4.2 per cent. Passenger numbers on the West Coast Main Line (WCML), which HS2 will relieve, have grown even faster.

“Since the upgrade was completed (in the mid-2000s), the WCML has seen a period of extraordinary growth and this has continued every year since – despite the economic downturn from 2008. Passenger journeys have nearly tripled, growing from 13.2 million in 1996/97 to 39.5 million in 2018/19, representing growth of 199 per cent since 1996/97 compared to 119 per cent on the wider rail network.”

At each point an increasing weight of evidence has demonstrated the pressing importance for a step change in capacity.

DfT

The DfT concedes that “overall demand growth at a national level has plateaued in recent years”. The annual growth rate for franchise operators was 3.7 per cent for 1994/95 to 2018/19 but 2.1 per cent for 2013/14 to 2018/19. Franchised long distance operators saw growth of 4.2 per cent in 1994/95-2018/19 but 2.6 per cent in 2013/14 to 2018/19.

The fast lines on the four-track at the southern end of the West Coast Main Line now carry 15-16 trains an hour in peak periods. “This is a higher intensity of operation than comparable major fast lines in other European countries, including purpose-built high-speed lines. The WCML has exhausted its available train paths and no extra services could be run without further significant investment to enhance current infrastructure or build a new line.”

HS2 will have capacity for “up to” 18 trains per hour. “Research from the University of Birmingham states that, under perfect conditions, 16 trains per hour capacity could be obtained on a high-speed line like HS2, without including recovery time. If automatic train operation was provided one to two more trains per hour is possible.”

The new railway will free up capacity on the southern end of the WCML for more local trains to places such as Milton Keynes, Northampton and Rugby. “Under current plans there will also be a substantial increase in the number of peak-time seats out of Birmingham, Manchester and Leeds.”

Under “current plans” HS2 could also ease pressure on the East Coast Main Line (ECML) and Midland Main Line (MML). This requires construction of Phase 2b, which facilitates London-Sheffield, London-Leeds Edinburgh/Newcastle/York-London services to run over HS2 infrastructure. This, in turn, would allow more local services on the southern end of the ECML between London and places such as Cambridge and Peterborough. The use of the words “current plans” may ultimately prove significant. Doug Oakervee’s review of HS2, published in February, raises questions about constructing the HS2 phase 2b connection to the Leeds-York line ( (LTT 17 Apr). Without it, Edinburgh/Newcastle/York-London services would all remain on the ECML.

HS2’s contribution to the economy has been a bone of contention ever since the project was first touted. Advocates say it will reduce the north-south economic divide; critics say it will reinforce the dominance of London.

“Improved connectivity and the associated agglomeration effect will boost regional economies by encouraging businesses to settle outside of London, helping to level-up the economy,” says the DfT. The evidence it presents includes comments by the CBI’s director of infrastructure, Tom Thackray, last August that approval of HS2 Phase One had already “led to record levels of foreign direct investment in the West Midlands, with more than 7,000 new jobs created in Birmingham as a direct result of HS2, and over 100,000 more. We have seen and are continuing to see similar benefits right across the proposed route.”

The DfT adds: “Key players in the services industries, such as HSBC and Channel 4 have already moved their headquarters to Birmingham and Leeds. In January 2020 BT Group announced it will take occupation of the Three Snow Hill development in Birmingham City Centre, in the largest single office letting in Birmingham, securing a reported 4,000 jobs.”

HS2’s contribution to the Government’s climate change agenda has been hotly disputed. The business case says HS2 has a “vital role” to play in achieving the Government’s Climate Change Act net zero greenhouse gas target for 2050. “HS2 has the potential to take passengers off domestic flights and reduce the demand for new roads.” It is predicted to deliver emissions of 8g per CO2e per passenger kilometre by 2030, compared to 22g by normal intercity rail, 67g by inter-urban car, and 170g by domestic aviation.

Improved connectivity and the associated agglomeration effect will boost regional economies by encouraging businesses to settle outside of London.

DfT

HS2 will consume about one per cent of UK electricity per annum, the DfT believes.

The greenhouse gas emissions associated with building HS2 are “significant”, the Department concedes, but it is keen to put things into perspective. “The estimated total carbon emissions from both building and operating Phase One for a full 120 years produces the same amount of carbon as just one month of the UK’s road network.”

The costs

It was last summer that the Government admitted what most people had long suspected – that the project was way off schedule and budget.

The Department now has more confidence in the latest costing of HS2 Phase One because it is informed by “mature design and contractor costs”.

“Following extensive challenge and benchmarking against comparable UK projects, the Department and HS2 Ltd now consider these estimates, including the contingency allowed, to be realistic.”

The previous baseline cost for Phase One relied 97 per cent on client-derived costs. The new version prepared last year (known as Baseline 7) is based on just under 50 per cent market prices from contractors, 28 per cent from HS2 Ltd’s professional service consultants, and the remainder from HS2 Ltd’s own estimate of the costs. “This difference in design maturity is a reflection on where each ‘cost pillar’ falls in the programme, with civils and stations work starting ahead of railways systems, rolling stock and the operational testing work that forms part of the final delivery stages,” the DfT explains.

HS2 Ltd awarded two-stage design and construct main works contracts for Phase One to four joint ventures in 2017 (LTT 21 Jul 17). Last month’s notice to proceed gives HS2 Ltd the authority to proceed to the construction stage.

The Oakervee Review suggested there might be benefits of reprocuring the main works contracts to achieve better prices. The DfT says this was unnecessary, however. “Prior to notice to proceed, HS2 Ltd closed on an agreed position on price, contract form and incentives with all the joint ventures,” it explains. “The Department is content that the negotiated commercial positions agreed with the joint ventures are acceptable value for money, with an incentivisation package designed to deliver gain-share savings during construction and limit further cost exposure above the target price.”

The revised commercial model “provides a lower level of risk transfer in order to avoid disproportionate risk premiums,” the DfT explains. This, it says, “was a pragmatic response within market constraints, given that the best alternative was a two-year reprocurement with no guarantee of a better outcome on cost, incentives or risk allocation”. Project risks continue to sit with the main works contractors, with programme risks held by HS2 Ltd.

To set the £40bn target cost and the £45bn funding envelope for Phase One, the Government used reference class forecasting (RCF). “This assesses the historic outturn performance of a range of projects with similar characteristics to the project in question and considers what cost and schedule contingency would need to be applied to achieve a predicted outturn if the current project performed on average as well or badly as the range of projects in the reference class,” the DfT explains.

The RCF was carried out by Oxford Global Projects, a spin-out consultancy from the University of Oxford’s Saïd Business School. The consultant’s chairman and co-founder is the mega-project academic Bent Flyvbjerg.

The RCF exercise used a dataset of 526 projects. The Department complemented the RCF analysis with HS2 Ltd’s quantitative cost risk assessment.

The £45bn funding envelope is based on RCF at the P75 (75 per cent probability) delivery confidence, which added approximately 37 per cent to costs to go. This equates to £10bn of contingency and would provide for sufficient funding for potential cost overruns in 75 per cent of the reference class sample. “The Department considers it is uneconomic to allocate additional funding beyond this level,” says the business case.

The £40bn target cost is calculated by taking the Phase One point estimate (£34.7bn) and adding contingency based on a P50 delivery confidence from the reference class forecast, an 18 per cent adjustment on the costs to go, approximately £5bn.

Because the business case is for Phase One, it is light on detail about the costs of phases 2a and 2b. Last summer the Government put the capital cost of the whole Y network at £81bn-£88bn in 2019 prices (LTT 13 Sep 19). The Phase One business case cites a central cost estimate for Phase 2a (West Midlands-Crewe) of £4.4bn plus 36 per cent contingency, taking the figure to £6bn. For Phase 2b (Crewe-Manchester and West Midlands to Leeds) it cites a central cost estimate of £28.7bn plus 36 per cent contingency, taking the cost to £39bn. These figures will be even less robust than the Phase One costing because the planning of phases 2a and 2b is less advanced.

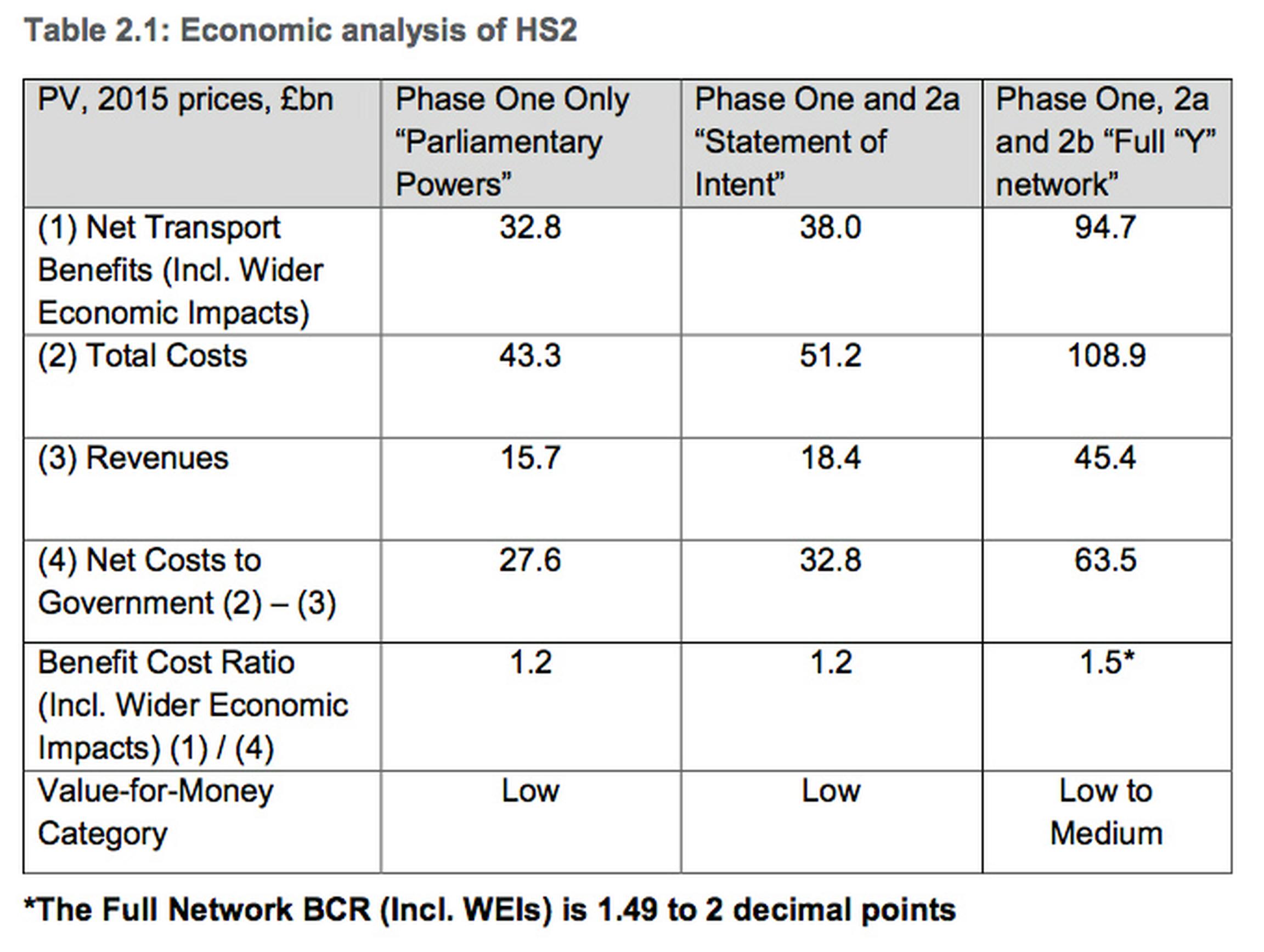

The economic case is complicated by the fact that results are presented for three different programmes. The first is the Phase One Parliamentary powers for a route between London and the West Midlands. In this scenario, trains to/from northwest of England trains would join/leave the WCML at the proposed Handsacre Junction. The second economic appraisal considers the Government’s ‘statement of intent’ to build HS2 Phase One and 2a (West Midlands to Crewe) to the same schedule, eliminating the need for trains to join the WCML at Handsacre. And the third appraisal considers the whole Y network.

The headline numbers from the economic appraisal are that Phase One has a benefit:cost ratio of 1.2, representing low value for money. This BCR is calculated both for the HS2 Phase One only and for the Phase One and 2a combined, though the numbers underpinning the ratio differ.

The BCR for the whole Y network is 1.5, the border between low and medium value for money.

It’s worth remembering that, in line with Government guidance, these BCRs ignore sunk costs – expenditure made on the project up to the end of 2019 (except for purchase costs on land and property that could be recoverable were HS2 not to go ahead). The total spend on HS2 so far amounts to about £8bn.

The above BCRs take into account both transport user benefits and wider economic impacts (WEIs). The DfT’s appraisal guidance nowadays identifies three levels of scheme appraisal, varying by the maturity of their techniques: user benefits (most mature); wider economic impacts (WEIs) assuming fixed land-use; and variable land-use (least mature).

The DfT and HS2 Ltd plan to prepare an economic case based on variable land-use for future business case updates. The DfT points to the importance of land-use change to the project’s strategic case – for instance, regenerating city centres and creating new business activity around out-of-town stations such as Birmingham Interchange and Toton.

Using the standard 60-year appraisal, the assessment of phase one and 2a combined produces net transport benefits of £30.3bn. The main ones are: journey time reductions £17.7bn; reduced crowding £5.1bn; and greater reliability £4.35bn. WEIs add a further £7.7bn.

Acknowledging that the Phase One BCR represents low value for money, the DfT emphasises that Phase One is “an enabler to the full Y network, which has demonstrated ‘low to medium’ value for money]”. Moreover, “switching values and sensitivities demonstrate that only small changes to the benefits or costs of the full ‘Y’ scheme move the BCR to a medium value for money, i.e. above 1.5:1”.

Conversely, further cost increases or lower demand/WEIs, or a combination of the two, could push the BCR down further. If the whole of the funding envelope is needed, i.e. £45bn, then the BCR of Phase One falls to 1.0 with WEIs (poor value for money is anything below 1). A 16 per cent drop in user benefits and WEIs would push the BCR for Phase One down to 0.9.

The Department has conducted a number of sensitivity tests on the economic case. In the conventional appraisal, the HS2 passenger demand forecasts are capped to the rate of population growth from 20 years after the start of the appraisal period, in line with the DfT’s Transport Appraisal Guidance (TAG). This results in the cap applying from 2039/40, shortly after the full Y-network becomes operational. An ‘Extended BCR’ sensitivity test extended the project’s demand forecasts.

“Whilst the demand cap reflects that the future is inherently uncertain, evidence suggests that demand growth is highly likely to exceed four years and to assume otherwise would fail to capture the effect that Phase 2b will have on the demand for rail travel,” the Department explains. “Thus, the application of a much lower growth rate from 2039/40 reduces the benefits and revenues captured in the economic case.

“Extending the demand forecasting period for an extra ten years will allow for more demand on Phase 2b with passengers benefiting from the faster, more frequent, more reliable and less crowded services. This approach forecasts demand growth of 0.6 per cent per annum (itself a conservative estimate) above population growth for the ten years to 2049.” This raises the BCR for the Y network to 1.8.

HS2 chairman Allan Cook’s report on the project last year recommended that an appraisal lasting longer than 60 years be conducted (LTT 13 Sep 19). The DfT has tested this out with a ‘residual value sensitivity’. “HS2 is currently appraised over a standard Departmental TAG 60-year appraisal period although it is expected to be operational for considerably longer,” the DfT explains. “The country’s existing rail network was first developed by the Victorians and continues to be used today. Indeed, HS2 Ltd is required to design the infrastructure for a 120-year design life.

“By assessing the benefits, revenues and operating costs over 100 years they are closer aligned to the [railway’s] design life of 120 years. Inclusion of the residual value sensitivities increases the BCR to 1.8 [a table in the report gives a value of 2.1] when including WEIs, which pushes the value for money into medium.”

The combination of a 100-year appraisal and extending the demand forecasting period by ten years to 2049 raises the BCR for the Y network to 2.6.

The DfT expects that HS2 will lead to an improvement in the financial position of Britain’s railways.

“Our analysis suggests that this could range from around £170m (Phase One) to £670m (Full Network) per year.”

The Government has yet to decide how these extra revenues will be recovered.

“This will depend on future decisions on the operating and commercial model for HS2. To recover some or all of this surplus via the Infrastructure Manager [initially HS2 Ltd], the Government intends for HS2 Ltd to levy an investment recovery charge on all operators using HS2 infrastructure.

“The charge is essential to preserve the option of a future concession sale of HS2, as it provides an income to the infrastructure manager that is over and above the direct costs it incurs. Without such an income stream the concession sale value of HS2 will be insufficient for this to be a credible option.”

With an investment recovery charge in place on HS2, the Government will have a choice between the early sale of a concession to raise significant funds upfront, or to retain ownership of HS2 and take the surplus revenues as an ongoing income stream.

An investment recovery charge applies on HS1, the Channel Tunnel Rail Link. Its completion in 2007 was followed three years later by the Government letting a 30-year infrastructure concession. Explains the DfT: “While the Government has not decided at this stage whether to pursue a similar model for HS2, retaining the ability to sell HS2 as an infrastructure concession is an essential requirement for the programme, and HS2 Ltd is instructed in its development agreement to ensure that this option remains available.”

The management case for Phase One explains how the Government intends to ensure the project is delivered smoothly. The HS2 Ltd board is to be strengthened, including by the appointment of at least three further non-executive directors to bring in new challenge and leadership. Two will be nominated by the Government to represent its interests and to act as a direct link back to the Department.

“HS2 Ltd intends to make changes to its executive to reflect the delivery model following notice to proceed,” adds the DfT.

The DfT is the sponsor for the HS2 programme, responsible for setting the policy framework, securing the funding, and ensuring that the benefits are realised. Andrew Stevenson is the transport minister responsible for HS2 and an HS2 ministerial committee is being set up too. The programme is led by the Department’s director general for the High Speed and major rail projects group (HSMRP), who is also the programme’s senior responsible owner (SRO). Beneath this are four directors in charge of Phase One; Euston (to be appointed); Phase 2 and Northern Powerhouse Rail; and programme integration.

The full business case for HS2 supports the Government’s decision to go ahead with the entire new rail route from London to the cities of the Midlands and the North, despite the dramatic escalation in construction costs, from £37.5bn in 2011, to £50bn in 2013, to £65bn in 2015, to £109m1 in the latest business case, and doubtless even more in eventual outturn.

It is noteworthy that the initial increases in the cost of HS2 did not change the supposed economic benefits, as measured by the benefit-to-cost ratio (BCR), which held steady at close to 2.0, representing ‘high’ value-for-money according to the DfT’s value for money framework for economic appraisal.

This was the result of substantial additional benefits being recognised by the promoters, even though nothing fundamental had changed in the business case. However, last year independent reviews by Douglas Oakervee and by the National Audit Office estimated higher capital costs that reduced the BCR to 1.5 or lower.

The new business case recognises these new capital costs but fails to identify any compensating additional benefits, such that Phase One (London to Birmingham) has a central-case BCR of 1.2, while the full Y network has a BCR of 1.5.

Accordingly, Phase One has been assessed as ‘low’ valuef or money, while the full network would be ‘low to medium’. Any further increase in capital costs would reduce the outturn BCR, as would less demand than assumed for rail travel over the 60-year forecast period.

It is surely remarkable that the largest ever UK transport infrastructure investment is proceeding on the basis of such low returns, given the great number of more attractive potential such investments. Is this a case of politics trumping economics, or are the politicians right to see benefits not recognised by orthodox economic analysis?

The precedent of the Jubilee Line Extension (JLE) to London’s Docklands, with a BCR of less than one on the standard approach to appraisal, indicates the potential regeneration benefits that may be achieved. The increased real estate values, reflecting the economic benefits to businesses locating at Canary Wharf and beyond, were not taken into account since this would supposedly involve doubling counting benefits implicit in the value of travel time savings, the main element of economic benefit in the standard DfT WebTAG appraisal methodology.

These time savings comprise small amounts of time saved by large numbers of commuters, valued by market research techniques that require respondents to trade time and money in the short run. Yet it is scarcely credible that the aggregate of such time savings could provide a measure of the long run cumulative real estate value uplift, whether for the JLE or for HS2.

Moreover, orthodox investment appraisal has no spatial content, no indication of the geographical distribution of economic benefits. This is a crucial issue for HS2, the strategic aim of which is to boost the economies of the cities of the Midlands and the North.

More fundamentally, the importance attached to travel time savings is misconceived. The National Travel Survey has been measuring average travel time for 45 years, over which period it has hardly changed, despite many £billions of public investment in transport infrastructure justified by the value of supposed time savings.

In reality, people take the benefit of such investment not in the form of more time for work or leisure, but as greater access to desired destinations yielding more opportunities and choices. The purpose of HS2 is to increase the access to London of those living in the Midlands and the North (and vice-versa). Increased access will lead to changed land use and enhanced real estate values, which are the market indicators of economic development.

It is possible that the real economic benefits of HS2 are substantially greater than calculated in the full business case using the WebTAG methodology. It is therefore time to reconsider the basis of transport economic appraisal from first principles.

1 The £108.9bn is the estimate of total costs – capital costs, renewals and operating costs over the 60 year appraisal and is in 2015 prices. It is not therefore comparable to the £35bn-£45bn capital cost estimate of Phase One, which is in 2019 prices – Ed]

David Metz is honorary professor at the Centre for Transport Studies, University College London. He blogs at www.drivingchange.org.uk

TransportXtra is part of Landor LINKS

![]()

© 2025 TransportXtra | Landor LINKS Ltd | All Rights Reserved

Subscriptions, Magazines & Online Access Enquires

[Frequently Asked Questions]

Email: subs.ltt@landor.co.uk | Tel: +44 (0) 20 7091 7959

Shop & Accounts Enquires

Email: accounts@landor.co.uk | Tel: +44 (0) 20 7091 7855

Advertising Sales & Recruitment Enquires

Email: daniel@landor.co.uk | Tel: +44 (0) 20 7091 7861

Events & Conference Enquires

Email: conferences@landor.co.uk | Tel: +44 (0) 20 7091 7865

Press Releases & Editorial Enquires

Email: info@transportxtra.com | Tel: +44 (0) 20 7091 7875

Privacy Policy | Terms and Conditions | Advertise

Web design london by Brainiac Media 2020