Many of us have attended conferences on land value uplift (LVU) and capture (LVC) over the past 20 years that talk about the reality of LVU on infrastructure projects, making reference to the many studies that have measured it. Up until now though, no one has actually captured significant LVU, turning it into real LVC funds.

In the northeast of England, that has now changed. Working with Northumberland County Council, E-Rail has done it, securing between 25 and 30% of the capital funding required for the new passenger rail line from LVC. This is the first time this has been done in the UK.

We believe our method for LVC will be a game-changer for public transport investment. There are a significant number of rail projects, both heavy and light, around the UK that transport authorities want to deliver for local social and economic reasons. Funding for many of them has historically been constrained, and this will be exacerbated in the future, due to the unexpected government spending related to the Covid-19 pandemic and the consequential detrimental impact on the economic outlook. This constraint is contradictory, however, since after the pandemic the delivery of infrastructure will be a critical building block to economic recovery.

The concept of LVC is not new. It was used for the Canadian Pacific Railway completed in 1881, providing 12,500 miles of new track, and the London Metropolitan Line, 41 miles of underground and 34 stations, which opened in 1863. More recently, the Ørestad metro, which opened in Denmark in 2002, was also funded using LVC.

The historical schemes were done in an age of different planning and procurement rules and regulations, and the Ørestad project used land wholly owned by the Danish State and the City of Copenhagen. It is not so easy to do it here and now, given the necessary constraints of independence and discretion required by current procurement and planning rules and regulations, especially when seeking to secure contributions from multiple private sector landowners and developers interested in maximising their return.

There is also a problem of definition. In 2013 and 2014 I was asked by Metrolinx, the transport agency for the GTHA (Greater Toronto and Hamilton Area), based in Toronto, and the National Bank of Canada, based in Montreal, to produce comprehensive reports on all types of LVC methods. These reports divide the range of LVC methods into tax-based and development-based approaches. A number of these, especially the tax-based ones, have been successfully applied but they fall far short of securing the potential level of LVU that new rail-based services generate.

For example, Don Riley, in his 2001 book Taken for a Ride, calculated that the uplift in land and property solely due to the railway along the route of the Jubilee Line Extension in London was of the order of £13bn. The capital cost of the scheme was around £3bn but only a small contribution was secured, all from Canary Wharf. Most of the uplift created by the new line was not captured.

As a major property owner in that corridor, Riley benefitted from significant increases in value but argued that this wasn’t morally right since it was the taxpayer who had paid for the railway line. He suggested this created value should be shared between land and property owners and the transport provider. There have been at least two follow-on studies confirming his figures.

There are many more studies measuring land value uplift and four key points emerge from them:

So, having looked at the evidence, E-Rail spent many years developing a method of capturing and sharing this uplift created by a new transport facility between the provider of the service and the landowners and developers who benefit. The process was not easy, but we have now developed, tested and delivered a method that is unique in the UK. This article summarises the method we have developed and successfully applied in Northumberland.

Land and property within 1km of the construction of a new BRT, metro, light rail or heavy rail station increases in value. Existing house stock increases in value on average by 20 per cent. This is new money, which would not exist if the station and the service were not provided, and if land now ripe for development did not gain planning approval. There is a clear mutual advantage for both the transport provider and the landowner/developer, and thus an incentive for both in using this additional uplift to create the new station and service.

By sharing this generated increase in value, the transport provider gains significant funds that do not have to be paid back and the landowner/developer secures a considerable rise in property value.

This is why landowners and developers agree to participate in the arrangements, but it is not the only reason. One thing that has become clear on the Northumberland Line scheme is that landowners actually want to be seen to contribute to the project to allow it to be delivered, recognising the importance locally, regionally and strategically of the project.

The earlier that contributions agreements are reached, the earlier scheme certainty can be achieved and the more LVC can be generated. Such agreements, using our method, require no new legislation. They can be put in place right now, by any council or transport agency in the UK promoting a project.

The timing of the evaluation of LVU and securing LVC agreements is also important in relation to business case certainty. Evaluation should start early on, to ascertain the value of likely LVC and likely costs associated with securing agreement.

Contribution levels are assessed in Stage 1, to determine feasibility, and secured in Stage 2, through formal agreements signed by each landowner/developer (public and private) along the corridor.

The design and procurement process for the transport scheme and the planning process for any developments along the route are unchanged. It is imperative that the independence of the planning process and the procurement process are maintained and adhered to at all stages and the local authority and/or transport agency is in control of these processes at all times.

Our method can be applied to any fixed infrastructure transport scheme – heavy and light rail, metro, BRT, roads, bridges, ferries and potentially flood prevention schemes. It can apply to single stations or to large multi-station schemes where land value uplift will occur.

We believe our method for land value capture will be a game-changer for public transport investment.

Having developed our method, we needed to trial it on a real project. We approached a number of local authorities who showed great interest, a number of whom subsequently commissioned us to carry out initial Stage 1 assessments. However, Northumberland County Council (NCC) was the first authority to progress to the second stage and commission us to deliver LVC contribution agreements using our method. This is the first application of our LVC method from start to finish in the UK and globally.

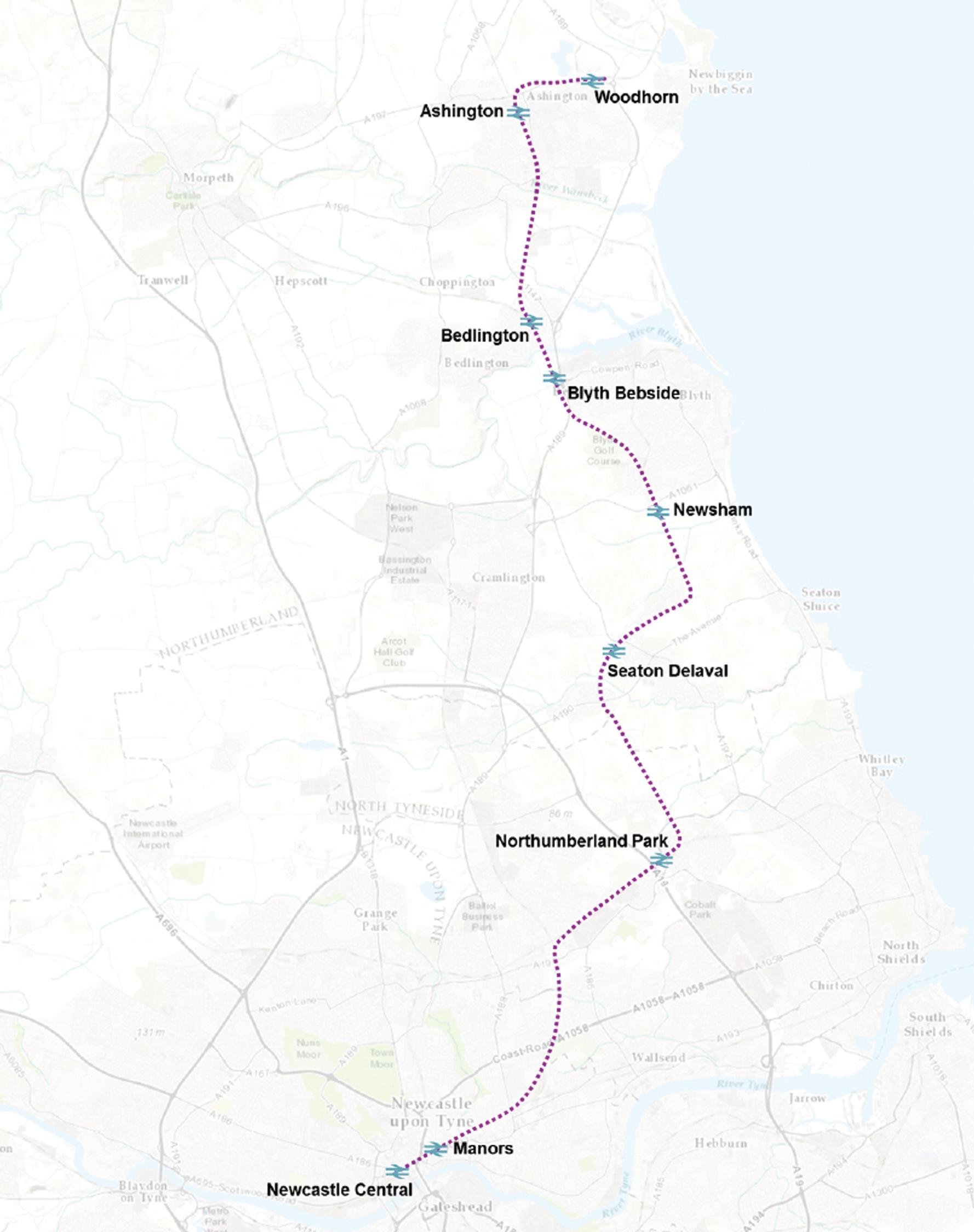

Our initial evaluation determined that the Northumberland Line was ideally suited to our LVC process. The line is at present a freight-only line running from Ashington to Newcastle via Bedlington, Blyth, the Seaton Valley and North Tyneside. The potential of re-opening the line to passengers is very significant and because of this it is NCC’s number one transport project. This is because it connects a large part of southeast Northumberland to North Tyneside, the Tyne and Wear Metro system, the international airport, Newcastle city centre and the East Coast Main Line. The social and environmental impact on this area will be substantial as the road network is congested and the public transport network is sparse. In addition, it will increase the accessibility of the area to the key areas listed above, thereby generating economic activity and raising land and house prices.

The other significant fact was that the scheme had been in development for many years, without being able to bridge the funding gap. A funding gap is essential for E-Rail because if the private sector believes the Government is going to fully fund a scheme anyway then it is very difficult to generate any LVC from landowners, except through tax-based planning charges with much smaller returns.

NCC progressed the project through the Rail Network Enhancements Pipeline (RNEP) process with the DfT and Network Rail. Through the business case and approval process, NCC continued to fund the project development, putting consents and design plans in place at risk. On 23 January the DfT announced the award of £34m for land acquisition, detailed design and preparatory works for the project. Northumberland will submit a full business case for the project to the Government in the autumn, which will hopefully lead to the release of funding for construction. Opening is expected in 2024.

The project will deliver a 30-minute service. It is assumed that the operator will be Northern Rail under the existing franchise.

The scheme is currently working through GRIP 4 outline design stage. Some additional track (loops and sidings) is included in the scheme, together with re-signalling. There are six proposed stations: Northumberland Park; Seaton Delaval; Newsham; Bebside; Bedlington; and Ashington. Northumberland Park will offer interchange with the Tyne and Wear Metro. The rolling stock is likely to be Class 158 diesel multiple units for the initial ramp-up period.

NCC has shown great vision and determination, whilst at the same time exercising prudence and assurance, properly checking and validating the results of each stage in great detail, including all legal and financial matters. This experience has helped us evolve the method, testing it in a live environment and with a diligent scheme sponsor.

The process was rigorously tested as it matured over a series of stages:

Having completed this process, we are now able to confirm that the method we have developed has moved past the proof of concept stage and we can confirm it works and can generate significant LVC contributions for transport projects. The percentage we can raise obviously varies by project, but the sum raised for the Northumberland Line, of between 25 and 30 per cent of the capital cost, would appear to be a good indicator of what to expect.

It is important to stress how this has only been possible because of the strategic and innovative foresight of NCC. NCC was willing to test our method to a conclusion where others were not.

Our LVC method can work in partnership with CIL, Section 75/106, tariffs and so on. Whilst our LVC value will be greater, you can’t ask for the money twice, so if any money is raised from these alternative options for the transport project then it would be deducted from the LVC contribution value. If the sums raised through more traditional methods are for other purposes, such as local road infrastructure, then that does not affect any LVC funding.

One of the major constraints with LVC generally is the time lag between funding the cost of the infrastructure works and receiving a share of the value uplift generated by the consequential development.

On commercial development schemes, developed for example through Enterprise Zones, local authorities often assess the potential future income streams, including risk, and where appropriate allocate capital risk funding against schemes on this basis. It therefore ought to be possible for a similar assessment to be made of LVC in order to underwrite initial capital requirements on transport projects.

An independent value calculation was made on the Northumberland Line scheme, to support our assertion of the likely uplift, and as part of the risk assessment process. This provided confidence with respect to the scale and veracity of the opportunity.

Where LVC is being used as a funding opportunity, a strategic rail upgrade (such as proposals being put forward for the DfT’s Restoring Your Railways funding) really ought to justify central government intervention in some way. Since the Green Book appraisal process includes for a calculation of land value uplift to justify providing DfT funding, it would seem rational for risk capital funding to also come from the DfT or the equivalent devolved agencies, against which future LVC receipts can be offset, and taxpayer funding repaid.

It is imperative that public funders should make a consideration of LVC during the early stages of scheme development (we would suggest at strategic outline business case stage). This delivers two key outcomes. Firstly, it establishes the opportunity for LVC (and preferably also secures it) as part of the funding package for a project early on, which increases the chances of the scheme actually happening. Secondly, it maximises the opportunity for participation in LVC by landowners/developers.

It would seem sensible for policy-makers to be considering what a process for securitising LVC on a risk-based approach might look like, as well as making the assessment of LVU and securing of LVC a mandatory element in any business case evaluation.

We would recommend that a policy to support LVC be developed by the DfT in partnership with the devolved transport agencies such as Transport Scotland, as a key element to be considered by scheme promoters. At present this does not happen at all.

Dr George Hazel OBE is a founder director of Edinburgh Rail (trading as E-Rail).

TransportXtra is part of Landor LINKS

![]()

© 2026 TransportXtra | Landor LINKS Ltd | All Rights Reserved

Subscriptions, Magazines & Online Access Enquires

[Frequently Asked Questions]

Email: subs.ltt@landor.co.uk | Tel: +44 (0) 20 7091 7959

Shop & Accounts Enquires

Email: accounts@landor.co.uk | Tel: +44 (0) 20 7091 7855

Advertising Sales & Recruitment Enquires

Email: daniel@landor.co.uk | Tel: +44 (0) 20 7091 7861

Events & Conference Enquires

Email: conferences@landor.co.uk | Tel: +44 (0) 20 7091 7865

Press Releases & Editorial Enquires

Email: info@transportxtra.com | Tel: +44 (0) 20 7091 7875

Privacy Policy | Terms and Conditions | Advertise

Web design london by Brainiac Media 2020