The pace of change in the UK mobility landscape is arguably now the fastest ever. Even the arrival of the railways took a couple of decades to begin to change the face of our countryside and urban geography. Likewise the impact of the motor car, which began with driving being a very minority activity amongst the well-off for quite a long time. In contrast,the past twelve months, let alone the last few years, have seen major developments in all parts of the personal mobility sector. From shared bikes and cars to trends in motoring and conventional public transport use there is much change in the air, and in the way the different modes inter-relate, and may coalesce even more in the near future.

Publication of the second annual LTT/Landor Survey of Mobility as a Service in the UK this month comes at a time that the idea of MaaS itself has firmly taken root at national and local level. The House of Commons transport committee has held an inquiry into MaaS (its report is due shortly), and MaaS is one of the themes of the call for evidence linked to the Government’s Future Mobility Grand Challenge. People can now travel using the Whim MaaS app and subscription in Birmingham, and trials of MaaS design and technology are underway elsewhere.

The larger picture, however, of transport expenditure in the UK, reminds us that our travel is still currently predominantly car-based. Households spend in the order of £100bn a year on motoring compared to somewhere around £12bn on bus and rail fares (excluding subsidies).

The automotive industry, however, thinks this is likely to change. Car sales have been weak since the 2008 economic crisis and studies show that younger people have a declining interest in owning vehicles or indeed learning to drive. In response, car manufacturers are investing heavily in exploring new business models including shared transport, car clubs and peer-to-peer car sharing.

The automotive sector is not the only one sensing changes in mobility patterns. With a potential shift in expenditure, numerous players are lining up bids to redirect this flow of money into their businesses. The flag-bearer of these is Uber, which has attracted fares away from both traditional private hire and public transport as well as building a solid customer base amongst those younger people less likely to drive themselves and wanting a quick and cheap on-demand 24-hour mobility solution.

Lined up behind Uber looking at the potential to disrupt the market are mobile phone companies, the digital technology sector, and banking and finance. With smartphone use almost ubiquitous, whole new sectors are able to obtain information about people’s travel patterns, analyse this data and identify opportunities for new services. The travel data obtained by map apps (Google and Apple maps), other travel information apps (e.g. CityMapper) or by any app with location services always or even partially on (for instance a banking app) is incredibly rich and informative.

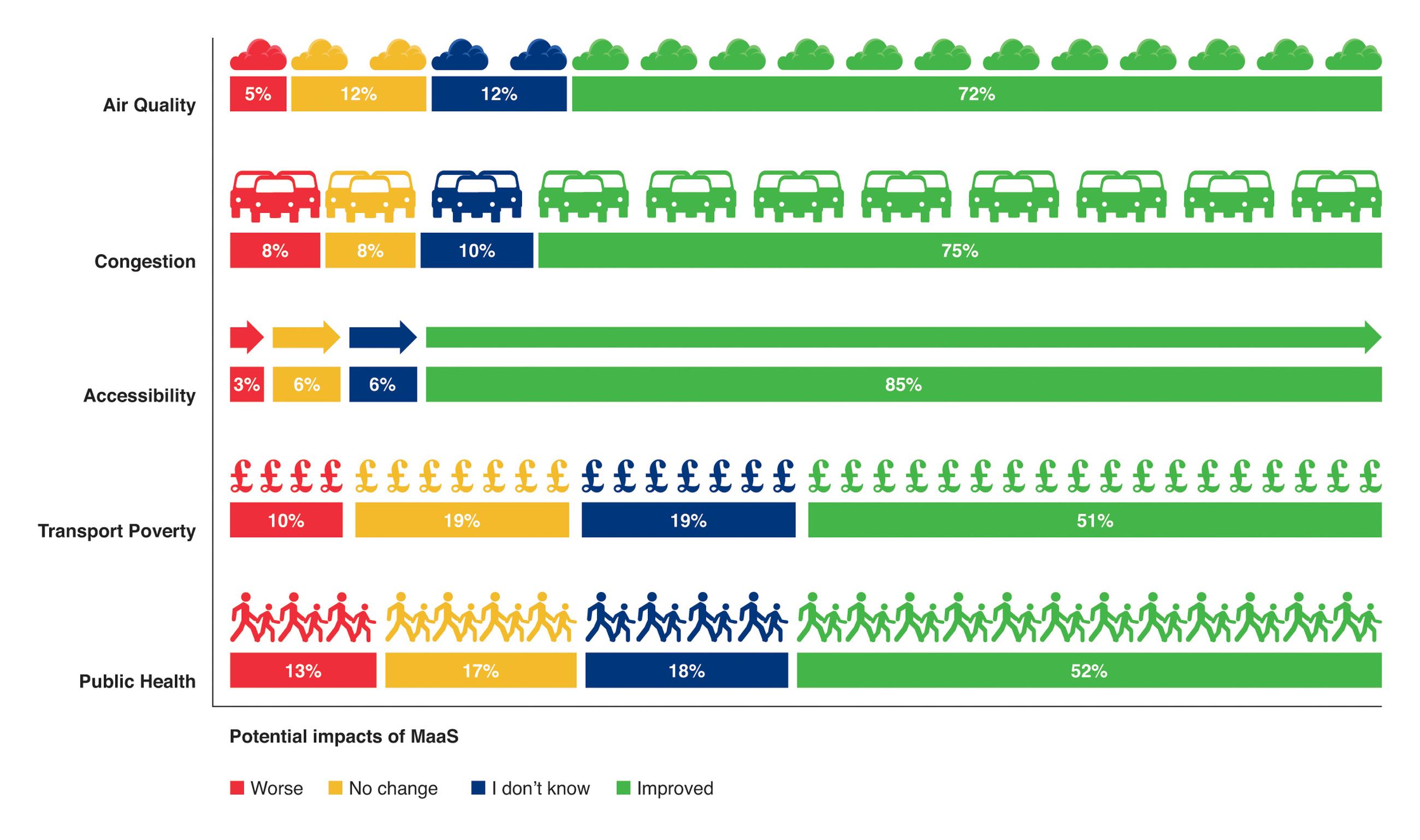

This year’s annual survey of MaaS developments in the UK has found that there is great enthusiasm and high expectations for MaaS amongst transport professionals. The vast majority of respondents we spoke to expect it to increase use of public transport (however defined) and decrease use of the private car – as well as having a positive impact on accessibility, congestion and air quality.

This enthusiasm is based on a particular view of MaaS as integrated, multi-modal travel. However, deeper analysis shows that those most enthusiastic about MaaS are those planning and managing transport in government (local, regional and national) and those advising them. Expectations are markedly less positive among the responses from those working for public transport operators, for example.

Whereas transport planners anticipate that public transport will be central to MaaS provision, bus operators are sceptical about the concept and whether it will benefit them. It appears there is a fairly fundamental stumbling block on the road to MaaS provision coming out of the public transport world. This scepticism, and a wish to defend the traditional business model, could turn out to be a mistake as the game changes around operators already finding the going tough in terms of financial performance.

Despite this, the survey outlines a number of MaaS trials involving the public transport sector. They cover a wide variety of scenarios and diverse user groups, from Manchester to Dundee. These provide interesting insights into consumer behaviour when provided with MaaS – as well as a number of different social and business cases for MaaS provision.

Whilst there are differences between the trials, they all show that people will increase their use of public transport (and particularly buses) if offered a cheap, convenient package which gives them control over their travel. Despite this mounting evidence, operators still appear to be concerned that MaaS will increase business costs whilst not being founded on a strong business case.

Where will the spending go?

Another question the report considers is that of transport capacity. If travel spend in the UK switches away from personal motoring – the question is, where will it go? Even a few percentage points of change represent billions of pounds. Where and how will the capacity increase commensurately in order to enable people to reach employment, education and services as well as enjoy leisure, travel and see friends and family? The business opportunity identified by the disrupters looking for sufficient volume may not always match up with all the demand and needs.

In the survey we document case studies that demonstrate that there are multiple new modes (or new ways of accessing traditional modes) entering the market. Some are based around making better use of cars, others remodel bus services or create ‘micro transit’ offers. A new breed of shared taxi to bus ‘feeder’ services have sprung up – largely initiated by bus operators. There has been an explosion of bike share (even despite the withdrawal of some dockless schemes there is still a greater spread of access to bike share than last year).

How these new services are accessed is interesting – some of these new modes are already integrated with MaaS platforms, some are prepared to integrate and others prefer to stand alone.

We are seeing multi-modal platforms emerge. For instance, as Uber capitalises on its hard-won customer base by adding services including bike share, peer-to-peer car hire and public transit ticketing (in the US) it is shifting from ‘taxi app’ to multimodal platform, and openly talking the language of MaaS. It’s hard to imagine that other platforms will not develop similarly.

Such developments cut across the survey respondents’ concept of MaaS, which point to an expectation of centrally planned city- or region-based services. The Transport for Greater Manchester trial, for instance, assumes a vision of better use of public transport and increased active travel. Transport for London sees its Oyster scheme as MaaS – despite the fact that it has not added any of the new modes to its offer.

These parallel developments point to MaaS platforms being potentially quite diverse. Their development will be at the interface between private investment, regulation and the needs of people for mobility.

The trajectory of development will depend very much on legislation and regulation as well as business model. One clear need that emerged from the survey was for open data and for a level playing field between modes in the provision of open data.

Our survey respondents were clear that a more solid and clearly defined vision and direction for MaaS is needed from public authorities nationally and locally.

MaaS is part of the testing and proving ground for new mobility business models. As the automotive sector looks at new business models, banks, mobile phone and digital technology companies seek to capitalise on the vast amounts of data they now have about consumers, and their huge financial muscle power, further disruption is likely, indeed almost inevitable.

Copies of the 2018/19 Survey of Mobility as a Service in the UK are available in print and digital forms for £125 + VAT and £45 + VAT respectively from www.landor.co.uk/maas. For general enquiries about the report contact Darryl Murdoch – Publishing manager on 0207 091 7891 or darryl@landor.co.uk

TransportXtra is part of Landor LINKS

![]()

© 2026 TransportXtra | Landor LINKS Ltd | All Rights Reserved

Subscriptions, Magazines & Online Access Enquires

[Frequently Asked Questions]

Email: subs.ltt@landor.co.uk | Tel: +44 (0) 20 7091 7959

Shop & Accounts Enquires

Email: accounts@landor.co.uk | Tel: +44 (0) 20 7091 7855

Advertising Sales & Recruitment Enquires

Email: daniel@landor.co.uk | Tel: +44 (0) 20 7091 7861

Events & Conference Enquires

Email: conferences@landor.co.uk | Tel: +44 (0) 20 7091 7865

Press Releases & Editorial Enquires

Email: info@transportxtra.com | Tel: +44 (0) 20 7091 7875

Privacy Policy | Terms and Conditions | Advertise

Web design london by Brainiac Media 2020