When I was invited to write the first Annual Survey of Mobility as a Service in the UK I was intrigued. Could you really survey something in such an early state of development? We currently only have one single ‘full’ Mobility as a Service (MaaS) application under active development in the UK. This app combines a number of public and shared transport operators and offers them through a single interface. A second is in the pipeline, but it will be at least a year in development. Trials abroad have taken some time to implement – and have had mixed results.

However, there is no lack of interest in, conferences about, or discussions of MaaS. Several organisations have sprung up to help the concept take root and come to market. It is a year since the Transport Systems Catapult published its milestone report: Mobility as a Service: Exploring the opportunity for MaaS in the UK.

What is MaaS?

The definition of MaaS is still quite conflicted. Descriptions vary depending on who you speak to. For the report, we surveyed industry definitions. The principle areas of agreement were that MaaS would include integrated payment systems and integrated journey planners. Beyond that, the consensus dissolves. The Transport Systems Catapult definition, for reference, is: “using a digital interface to source and manage the provision of a transport-related service(s), which meets the mobility requirements of a customer”.

Under this definition a single app such as Uber or Mobike could be viewed as MaaS, or a travel booking tool such as Opodo. However, this is not the universal expectation of what MaaS will be. Three sectors – the public sector, transport providers, and the automotive industry demonstrably visualise different endpoints for MaaS.

Transport planners’ expectation is that MaaS will enable personal travel planning version 2.0. Their response to our survey implies they believe that offering digital access to transport will precipitate desirable behaviour change. Likewise urban planners have modelled versions of MaaS and see the potential in it to reduce the number of cars on our streets and the vast areas given over to parking, enabling a reimagining and reapportioning of public space.

It’s almost axiomatic that ‘disruptive’ transport providers are interested in MaaS. Car clubs, bike share, ride sharing and all sorts of data-driven apps see a MaaS platform as a potential route to market for their services. The attraction for transport planning is that offering bike share, ride sharing or a taxi service alongside public transport provides ‘last mile’ travel options to facilitate better door-to-door journeys. The reality is that whilst some of these modes are keenly working on integration in the first MaaS trial in the UK, interestingly, one of the most advanced disruptive transport operators – Uber – is not participating.

MaaS as a business opportunity is a strong theme within the automotive sector. The new CEO of Ford, Jim Hackett, was appointed to put mobility at the core of the business. Ford is no longer a car maker, it’s a mobility provider. The industry abounds with trials of different mobility-based business models, from BMW’s DriveNow car club to mergers and multiple acquisitions bringing shared mobility into the automakers’ purvey. Whilst their immediate concern is the near future and the rise of service-buying in preference to ownership, they also have their eyes on the development of autonomous vehicles (AVs). The costs of development and production of AVs require rethinking the business models and routes to market for the entire industry. MaaS represents a coherent route to generating a return on their investment.

These interests are not necessarily aligned. They all represent quite different conceptualisations of the future. A best case scenario for the automotive industry is to optimise for car travel – possibly providing mobility as a service using a transport system based on fleets of autonomous pods – to preserve or grow income streams. On the other hand, transport planners see mobility as a service as offering seamless simple access to public transport, creating a transport system with minimal car use.

In writing the report, I surveyed and spoke to representatives from as many groups as possible.

As I researched views, my concern grew that the public transport sector was either ill-prepared, ducking the issue, or actively hostile. Emails went unanswered. Calls were not returned. It seems significant that Stagecoach was at this time making it known that it will not participate in the West Midlands MaaS trial.

Market potential

At every conference where MaaS is discussed someone will, at some point, wheel out the enormous size of the global transport market as a justification for taking aim at a section of it.

The optimistic new entrants see ‘plenty to go round’ in this vast number of trips, but incumbent providers will inevitably see this as a threat to their revenue streams. They are protective of their customer relationships – however dysfunctional these relationships are.

MaaS provides a forum in which to discuss ‘who owns the customer?’ and this is not a comfortable discussion for those who believe the customer is already ‘theirs’. Transport consultant Peter Warman was one of the few drawn to set this scepticism out directly in the report: “The introduction of a third party (or as I see it a virtual travel agent), other than from the public sector … merely results in added costs to the traveller or under-mining the profits of the operator...”

Whilst MaaS operators and transport operators are inching towards trialling MaaS, customers are rapidly developing their own idea about the transport they would like.

One only has to see the enthusiasm in Manchester for the new dockless Mobike system to see transport disruption happening. The rise of Uber and its ability to provide a brilliant customer interface and fully trackable, fast service, is a lesson for every student of behaviour change.

The rise of shared mobility in the form of car-sharing, ridesourcing, bike-sharing and crowdsourcing services, especially when combined with tech developments, provides an insight into the adoption of new mobility. The eagerness with which people adopt apps that make them feel in control, offer convenience, or cost savings, cannot be ignored.

However, the ultimate endpoint depends on whether these developments foreshadow greater behaviour change with people adopting more sophisticated integrations of public and share transport using apps – or whether entrenched business patterns stifle their development.

Put simply, could MaaS apps fail because public transport operators guard their relationships with their customers too closely?

This would not, of course, be a lasting endpoint. If MaaS apps offering broad transport modes – including public transport – fail, it is inevitable that disruptive alternatives will emerge and be adopted. If the space is left vacant, could we see the automotive industry vision of ‘public’ transport delivered by fleets of branded autonomous pods succeed?

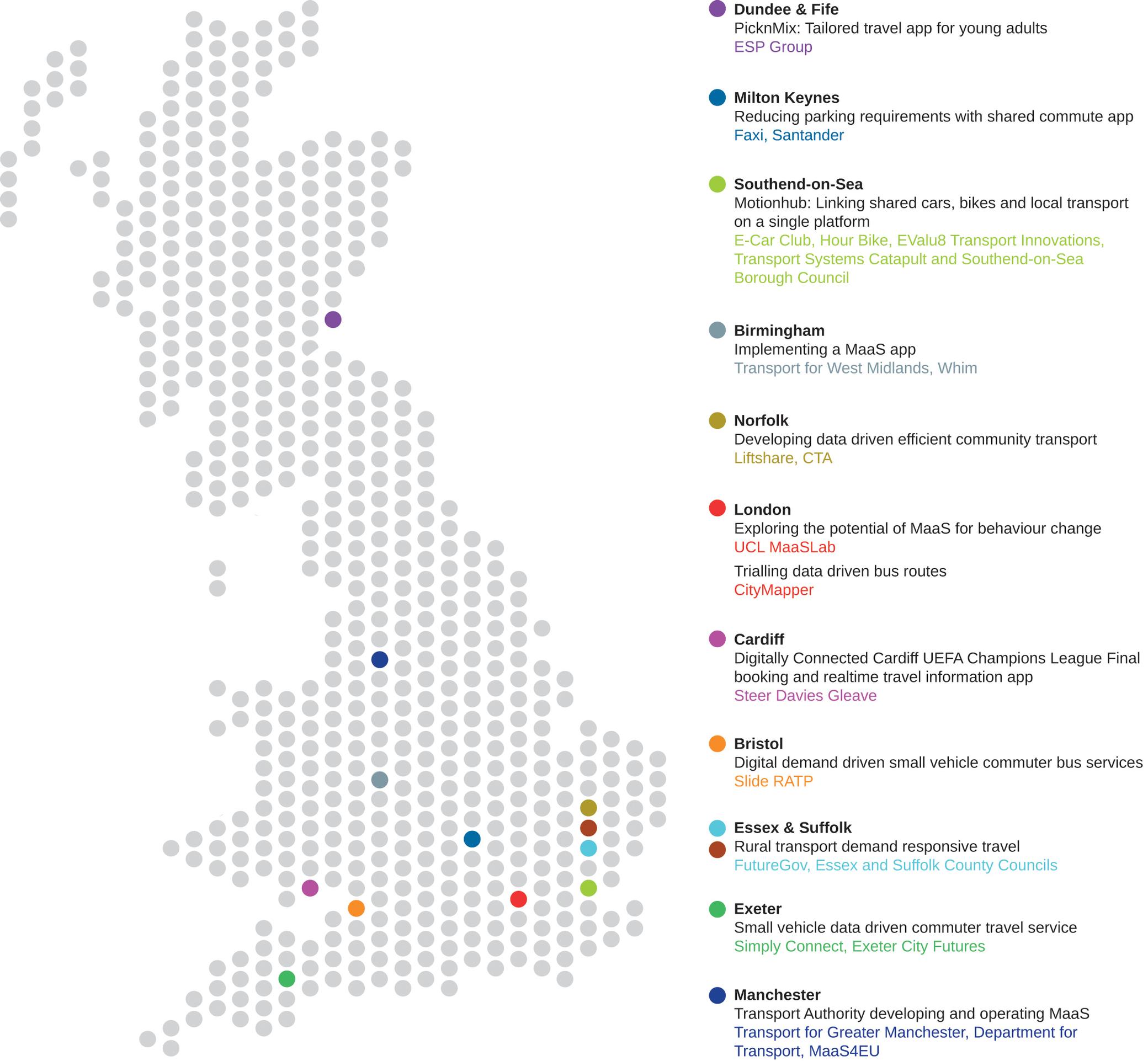

To see how likely these visions are, the survey looks at case studies across the UK.

Bottom up vs top down

My sense is that MaaS is developing in many ways both ‘spontaneously’ from the bottom-up and in an organised ‘top-down’ way. This can be seen in many dimensions – from the customer experience to transport operator co-operation and in the type of organisation that becomes the eventual MaaS operator.

There is a ‘build it and they will come’ approach in the West Midlands as MaaS Global works with Transport for West Midlands on a full transport provider solution providing most of the modes used by travellers in one app. In Scotland an app for young people provides travel information and calculates split taxi fares – after survey work found that’s what the potential users want.

Transport for Greater Manchester is embarking on creating a MaaS product offered by the authority. Other approaches can be seen in places such as Exeter where diverse solutions to pressing congestion issues are being trialled and operators are getting together to offer them on one app.

Data is possibly where there’s most convergence between ‘top down’ and ‘bottom up’ already. As regulation and legislation has forced rail and bus services to provide open data feeds these APIs (application programming interfaces) have become essential to travel planning. With Google’s policy of providing all publicly accessible transport on its map, it has become the go-to place for travel information for anyone with a smart phone. Services such as CityMapper have enough user data to predict the success of new bus routes and operate them. New modes are, by and large, keen for their feeds to be found in any travel planning app.

‘In between’

Researching the report revealed that there is a fertile ground of diverse innovative transport solutions that are somewhere between the disparate visions of MaaS.

The operators are various – they include those from the shared transport sector – car clubs, bike share and ride sharing; others that spring out of community transport; some are new operators; others occasionally traditional public transport operators trying new things; and they include tech companies. The vehicles involved include bikes, cars (including privately owned, shared or taxis) and mini-buses.

Some have been created to solve very particular congestion issues or to provide solutions to a transport problem, offer a better way of travelling to a particular user base or to change behaviour in particular area.

The key themes of these innovative transport solutions are that they are – to some extent – on-demand, flexible and data-driven. They generally reward people for making transport choices that have a better impact on congestion and air quality (compared with a one-person-one-car approach).

They provide opportunities for travellers to shift their behaviour and lead the way in demonstrating that there is an appetite for different modes of transport and different ways of accessing them.

When and how, not whether

Whatever happens, the status quo is unlikely to prevail. There are commercial pressures, legislative pressures, increases in population, technological developments and changes in consumer expectation converging on mobility. Air quality has to be tackled and there is legislative momentum behind plans to address it. The automotive industry has changed its business model from goods-based to service-based (over 80% of new cars in the UK are now leased rather than sold). Nothing is stopping the development of the autonomous vehicle.

My observation, having written and reflected on the report is not whether MaaS will happen, but which vision or version of MaaS will take root.

At the moment it is hard to make a prediction. The quiet skepticism of public transport operators currently indicates that they may be late to the game – allowing the automotive industry or other groups of new mobility providers to develop the market and embed their business models. However, a concerted development by one of the operators engaging with new mobility could change that.

Will some public transport operators take the initiative and start to bridge the gaps between innovative and traditional services? RATP or Arriva could look at ways of developing their trial small vehicle services and bundling them with other services or even other operators.

Could one of the shared transport apps such as Motionhub in Southend become a comprehensive transport solution? From the case studies researched there are clearly ambitions for smaller operators and shared transport to provide quick and light solutions which engage travellers. Could they provide apps that fulfill customer requirements for convenience, control and cost savings so that they don’t look to traditional public transport provision?

Ford in the US has rolled out a large bike share scheme and acquired an on-demand shuttle service. Could it – or another vehicle manufacturer – try developing a comprehensive combination of bike and car and ride share operations in a UK city?

The ghost in the machine

Obviously, nothing works if it’s not used by people. Smart phones are changing society in previously unimagined ways – and with 81% of the UK population carrying one around they can be considered mainstream. They enable everything from social connection to cost comparison.

With our access to knowledge has come – in my view – an increasing skepticism. We are increasingly incredulous at arcane systems, complex pricing and territorial boundaries. They are nonsensical in our connected world.

I strongly believe that the solutions that will be adopted will be those – like Uber – that cut through complexity and give us ‘get me there’ transport at the touch of a button. Whether Uber itself survives its own business model (it is currently rudderless, mired in scandal and burning billions of investor cash each year), it has created the perception that transport can be dialled up at the touch of an app, cheaply and securely. Operators that don’t recognise – and attempt to replicate – this, will be seen increasingly unfavourably.

This belief is substantiated by research into behaviour change undertaken in the Transportation Sustainability Research Centre in California by Modalgo, and by the University College London MaaSLab. Studies of travel behaviour and attitudes to MaaS indicate that convenience, control and pricing are the important drivers by which new mobility models will succeed or fail.

What these models will ultimately be, where they will be developed and who by is still not fixed.

The First Annual Survey of Mobility as a Service gives a flavour of the locations in which innovation is taking place, the operators engaging at present and the currents and controversies in the field.

My feeling is that the stage is set, but that nothing should be taken for granted. There is still room for surprise.

The First Annual Survey of MaaS in the UK is available in print and Kindle editions. To order copies visit www.landor.co.uk/maas

A website devoted to MaaS case studies is available at www.landormaas.blog

TransportXtra is part of Landor LINKS

![]()

© 2026 TransportXtra | Landor LINKS Ltd | All Rights Reserved

Subscriptions, Magazines & Online Access Enquires

[Frequently Asked Questions]

Email: subs.ltt@landor.co.uk | Tel: +44 (0) 20 7091 7959

Shop & Accounts Enquires

Email: accounts@landor.co.uk | Tel: +44 (0) 20 7091 7855

Advertising Sales & Recruitment Enquires

Email: daniel@landor.co.uk | Tel: +44 (0) 20 7091 7861

Events & Conference Enquires

Email: conferences@landor.co.uk | Tel: +44 (0) 20 7091 7865

Press Releases & Editorial Enquires

Email: info@transportxtra.com | Tel: +44 (0) 20 7091 7875

Privacy Policy | Terms and Conditions | Advertise

Web design london by Brainiac Media 2020